A mortgage Amortization calculator is a cutting-edge financial tool that enables the borrower to arrive

at an annual/monthly mortgage schedule. The calculator can help the borrower to differentiate between

the amount being paid towards the outstanding principal and interest.

Mortgage Amortization refers to the process of paying off debts by repaying the regular

interest

and principal amounts before the mortgage tenure reaches maturity. An amortisation mortgage

has

a fixed interest rate for its entire tenure.

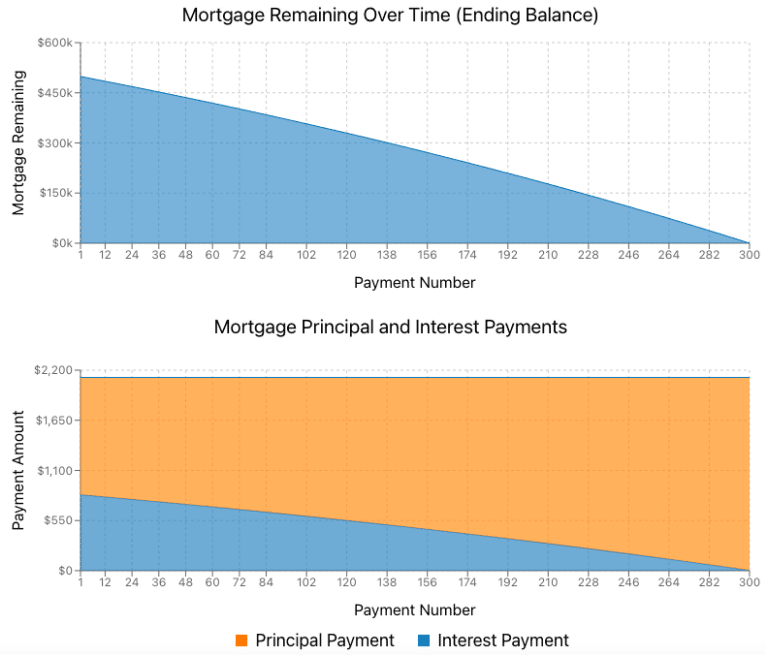

The primary characteristic of amortisation is that initially, a major chunk of your

EMIs

goes towards paying the interest amounts. But over time, as the interest amount decreases,

most

of your mortgage instalments go towards fulfilling your principal mortgage amount. An

amortisation is easier to manage than other debts as in it you know exactly when and how

much to

pay.

How to Calculate the Amortisation of a Mortgage?

An amortisation schedule lists the following items:

The principal and interest payable

The principal and interest that have been paid

The amount of principal owed on the maturity date

You can calculate the monthly amortisation amount by considering the mortgage amount and

interest rate.

Monthly payment= A [ I (1+i) ^ n / ((1+i) ^ n) - 1)]

What Do the Mortgage Amortisation Calculator Results

Mean?

The mortgage amortisation calculator offers results of multiple

variables with respect to a

mortgage.

Monthly Payment: The monthly payments include

how

much of the principal and interest amount you

are going to pay each month.

Total Principal Amount: The total principal

amount

is the total mortgage amount that you have

borrowed from the bank. It, therefore, equals the property price and closing costs (if any)

with

only the down payment amount subtracted.

Total Interest Amount: Covering a major chunk of

your mortgage cost, especially if you opt for a

full term of 15 to 30 years, is your total interest amount. To comprehend the true long-term

cost of borrowing, you can add your mortgage insurance premiums and closing costs to it.

Estimated Final Date of Payment: This is the

date

on which your mortgage tenure will mature.

Technically, it is the same date on which your mortgage amortisation starts. So, if your

mortgage amortisation of 30 years starts on May 1, 2022, its maturity date will be on May 1,

2052.

Running Total of Interest: It is the column in

the

amortisation schedule that shows you the total

interest amount you have paid in a year during your ongoing amortisation period. For

instance,

you have paid $5,000 in 2020, $7000 in 2021, etc.

Total Balance Remaining: This simply demonstrates the annual remaining

mortgage

amount that you

still have left to pay. It helps you understand how close you are to completing your

mortgage

repayment.

How to Speed Up Mortgage Amortisation?

Amortisation Periods: With shorter amortisation

periods, principal payments become higher, but the interest payable decreases drastically.

The

mortgage will be repaid earlier. This strategy should be used only if you can pay higher

instalments of the principal amount.

Extra Principal Payments: Longer amortisation

periods accelerate the payment. By using this method, you save more on interest. It adds

extra

payments to the monthly repayment. This strategy helps you become debt-free faster. For

example,

if a borrower has a $100,000 mortgage amortised over a tenure of 20 years with an rate of

interest of 6.45%, and they have repaid by paying extra principal, then they can save nearly

$30,000 over the mortgage term.

Lump Sum Payments: They are made in addition to regular payments to shorten

the

mortgage payment period. Such lump sum payments usually affect the earning potential of

banks;

therefore, the latter usually charge penalties or place limits on the maximum amount for

lump

sum repayments.

What is the Mortgage Amortisation Schedule?

A mortgage amortisation schedule is a table that shows the amount

of

principal and interest components payable monthly. As you keep paying off the mortgage, the

portion of the interest component gradually decreases, leaving only the principal component.

It

is displayed in a table format at the beginning of the mortgage.

Each row represents payment details for a single month. The rows are organised in

chronological

order, wherein the first row shows the first month’s details, and the last row lists the

last

month’s details. The mortgage amortisation schedule can be generated by using an

amortisation

calculator. It acts as a tracker for the borrower to monitor the amounts owed and repaid.

In straight-line

amortisation,

the interest payable is divided equally over the term of the mortgage. It is a simple method

as

the principal and the interest component payable are constant throughout the tenure.

Declining Amortisation

As the tenure of the mortgage

progresses, the interest amount payable decreases while the principal amount payable

increases.

In this case, the periodic payment is greater than the interest payment. Lower interest

rates

result in faster repayment.

Annuity Method

The annuity method in mortgage

amortisation includes numerous equal payments. Annuities can be classified as ordinary

annuities

and annuity dues. An ordinary annuity is paid at the end of each period as opposed to when

payments are made at the beginning of each period. The longer the mortgage tenure and the

higher

the rate of interest.

Balloon

In a balloon mortgage, the borrower repays

the

mortgage at maturity. The mortgage is repaid in small instalments, with a majority of the

repayment being made at maturity. As the tenure progresses, the outstanding balance

decreases

until it reaches zero at maturity.

Bullet mortgage

In a bullet mortgage, only the

interest

component is covered. At maturity, the entire principal is repaid. There is no change in the

outstanding mortgage balance during the term, and it is zeroed out at maturity.

Negative Amortisation

In this method, the total

payment

of the tenure is less than the interest payable during the tenure. Here, the interest

payable

gets accumulated and becomes outstanding.

How to Prepare an Amortisation Schedule?

An amortisation schedule contains the instalment amount,

principal

and interest payable over the mortgage tenure. The schedule is prepared in an Excel sheet.

Monthly Periodic Payments- The periodic payments are calculated via the Ordinary Annuity

method.

Monthly payment paid= I*PV/ 1- (1+i)^n

PV = present value of mortgage amount

I = interest rate

n = number of payments

The borrower has to pay interest on the mortgage amount during repayment of the mortgage.

I= P*I

P = principal

I = Rate of interest (in decimal)

Principal Amount Calculation: Interest and principal are the

components of the monthly payments. Hence, the principal amount is between periodic payments

and

interest.

For example:

mortgage: $200,00

Period: 36

Interest Rate: 6%

Period

Principal

Interest

Payments

Balance

1

$5084.39

$1000

$6084.39

$194,815.61

2

$5109.81

$974.58

$6084.39

$189,705.8

4

$5,153.36

$949.03

$6,102.39

$184,570.44

5

$6,024.00

$60.39

$6084.39

$6,054.12

6

$6054.12

$30.27

$0.00

$0.00

Monthly Payment= I*PV/ 1- (1+i)^-n

MP = 0.005* 200,000/ 1- (1+0.005)^-36

= 1000/0.16

= $6084.39

(Interest per annum is 6%. Hence, monthly interest is 0.06/12=0.005)

Interest Payable= P*I

I= 200,000* 0.06/12

= $1000

Principal payable= Monthly Periodic Payment - Interest payable

Principal payable= $6084.39 - $1000

=$5084.39

Balance= $200,000 - $5084.39

= $ 194,915.61

Other Calculator

Mortgage Amortization Calculator

Mortgage EligibiltyCalculator

Mortgage Payment Calculator - quickly calculate Monthly Mortgage Payment Online

at Urban Money Canada. calculate Mortgage Loan EMI, Interest Rate & lot more

Mortgage Amortization EligibiltyCalculator

Mortgage Amortization Calculator: Get a rough estimate of the principal and

interest component that you have paid by now. Find out monthly and annual

payments.

Land Transfer Tax EligibiltyCalculator

Land Transfer Tax Calculators - quickly calculate land transfer tax for Ontario,

Quebec, British Columbia, Alberta, Manitoba, Saskatchewan and Atlantic online at

Urban Money Canada.

CMHC Mortgage Insurance EligibiltyCalculator

CMHC Mortgage quickly calculate your monthly mortgage insurance cost with

Different Down Payments ,Also compare your mortgage insurance premium estimate.

FAQ’s

Ans. Amortisation is the time taken by the borrower to repay the mortgage. The amortisation primarily depends upon the current year

Ans. The mortgage term and mortgage amortisation can be different. Such a setup is called split amortisation.

Ans. Mortgage amortisation is easier to handle than other types of mortgages. The amortisation schedule helps you monitor payments already made and upcoming payments.